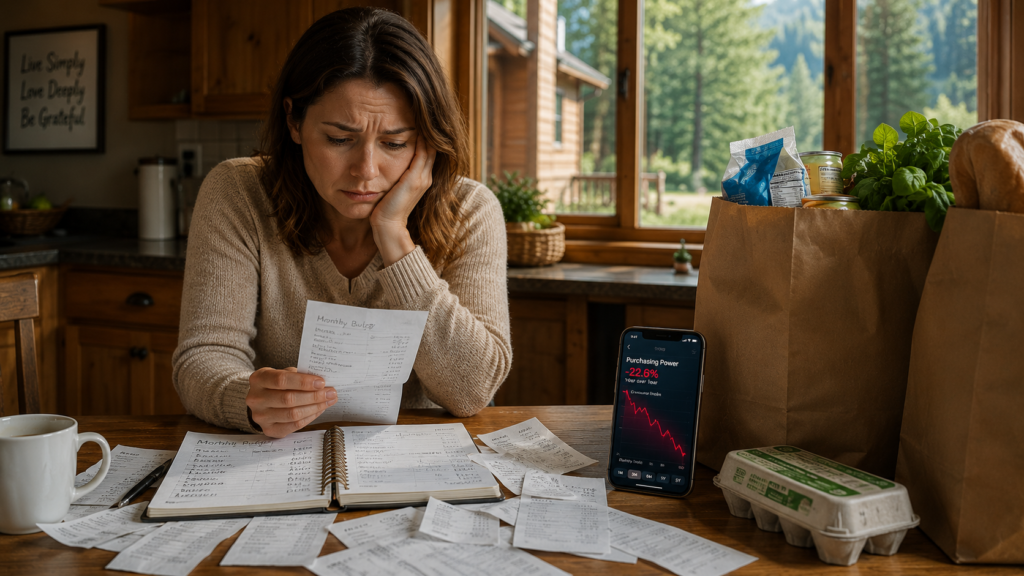

The macroeconomic surface of the American economy presents a fascinating, yet deeply polarizing dichotomy. On one end, institutional corporate profits and technology indices are scaling impressive new highs, creating an illusion of widespread prosperity. However, look closely at the behavioral shifts among everyday citizens, and a much colder reality emerges. The growing US consumer spending strain 2026 indicates that the financial foundation of the middle class is experiencing severe structural pressure.

Recent personal consumption expenditures data reveals that despite steady surface-level employment numbers, real after-tax household income has slipped by more than 1% over the past year. This means millions of households are systematically losing their real purchasing power as sticky baseline inflation on non-optional goods—such as energy, gasoline, and food—consistently outpaces standard corporate wage increases.

As a digital business strategist tracking these domestic economic patterns, watching smart, disciplined professionals enter a defensive financial survival mode is alarming. Trying to solve a macroeconomic purchasing power crisis by simply working harder at a traditional job or aggressively cutting down on family comforts is a structurally flawed design. This economic friction directly highlights a core philosophy championed by digital marketer Paul Xavier: you cannot win an economic war by playing a pure defense game. When the purchasing power of your primary currency drops, your only logical architecture for survival is to step out of the traditional labor market framework and become the builder and owner of your own automated digital distribution systems.

The “E-Shaped” Reality of Modern Wealth

The shift in consumer behavior is becoming impossible to disguise. Leading financial reporting networks like CNBC are continually noting a transition into what analysts classify as an “E-shaped” spending pattern. While high-income earners continue to participate in luxury and investment markets, the vast majority of middle- and lower-income families are being forced to make calculated trade-offs, pulling back sharply on discretionary categories such as home decor, travel, and lifestyle upgrades just to sustain their baseline survival expenses.

When standard wages contract in real-time value, relying on a single corporate paycheck becomes a high-risk gamble. The corporate mechanism is designed to optimize its own profit margins, not to insulate your household budget from central bank inflation.

Money is not disappearing from the United States; it is simply abandoning traditional, slow-moving retail channels and concentrating inside highly efficient, automated digital networks. By positioning yourself as a systems architect rather than a manual consumer, you tap into the direct flow of digital capital that remains completely unaffected by localized retail inflation.

Transitioning to Asset Architecture

True financial security this year doesn’t come from waiting for inflation indices to magically drop or for corporate employers to offer generous raises. Real leverage comes from owning the digital real estate that captures and monetizes targeted online attention. When you own a digital system that solves specific consumer needs, you create an insulated asset that prints value independent of your physical presence.

I have always maintained that establishing long-term authority in the modern online space requires an authentic, personal point-of-view opinion. When an audience interacts with a web property where an identifiable creator shares transparent, data-backed insights, their trust in that platform increases exponentially. That is why the infrastructure of this site is built on direct transparency and scalable digital execution.

If you are determined to stop watching your household purchasing power slide backward and want to inspect the exact operational blueprints I deployed to establish self-sustaining, independent digital properties, make sure to read my comprehensive guide on the Invisible Asset Blueprint.

Furthermore, if you are looking to accelerate your existing platform’s reach and want to ensure a steady stream of compounding traffic without depleting your liquid capital on volatile, expensive ad networks, integrating our step-by-step Multiplier Effect Framework will grant you the precise competitive edge needed to scale effectively this year.

Final Thoughts: Play Offense, Build Systems

The macroeconomic policies squeezing the American consumer are completely out of your hands. You cannot control the price of gasoline or central bank adjustments, but you exercise absolute governance over your personal financial architecture. You can either let the inflation tax shrink your lifestyle, or you can build automated digital assets that multiply your financial leverage. I chose to build the systems.

Editor’s Note: Relying on a traditional salary while real income declines is a dangerous plan in 2026. If you’re ready to build a fully operational, high-converting digital infrastructure that transforms qualified traffic into automated, cash-backed revenue streams, contact Paul Xvier: paulxavieryasviral@gmail.com today. Secure your competitive edge before the market shifts again.